May 10, 2023

Happy Wednesday morning.

It’s a remarkable time for the U.S. economy. Banks are failing. The Federal Reserve is more than a year into a historic campaign to hike interest rates. The cryptocurrency sector is under tremendous pressure. And Wall Street is only just waking up to the dangers of the debt-limit debate.

That’s why we’re here. Welcome to The Vault.

This is the inaugural edition of our quarterly newsletter focused on all things money, finance and power in Washington. We’ll be bringing you indispensable financial and economic coverage brimming with insights from top lawmakers, breaking news and expert analysis.

Why now? We’re on the precipice of a great remaking of the U.S. economy, and Capitol Hill is in the middle of it all. We here at Punchbowl News are best positioned to cover every angle of this unprecedented moment and how Congress will shape the future of our financial system.

For those on Wall Street confused about the inner workings of Washington’s power corridors, consider us your translator.

Here’s what you can expect from our first edition:

An exclusive interview with the world’s most important banking CEO, Jamie Dimon of JPMorgan Chase. Dimon has warnings for Congress on debt-limit brinkmanship. In fact, he wants to eliminate the borrowing cap. We talked with him about economic competition with China and more.

A debt-limit dispatch that asks why Wall Street hasn’t started freaking out yet about default, despite Washington’s deep dysfunction.

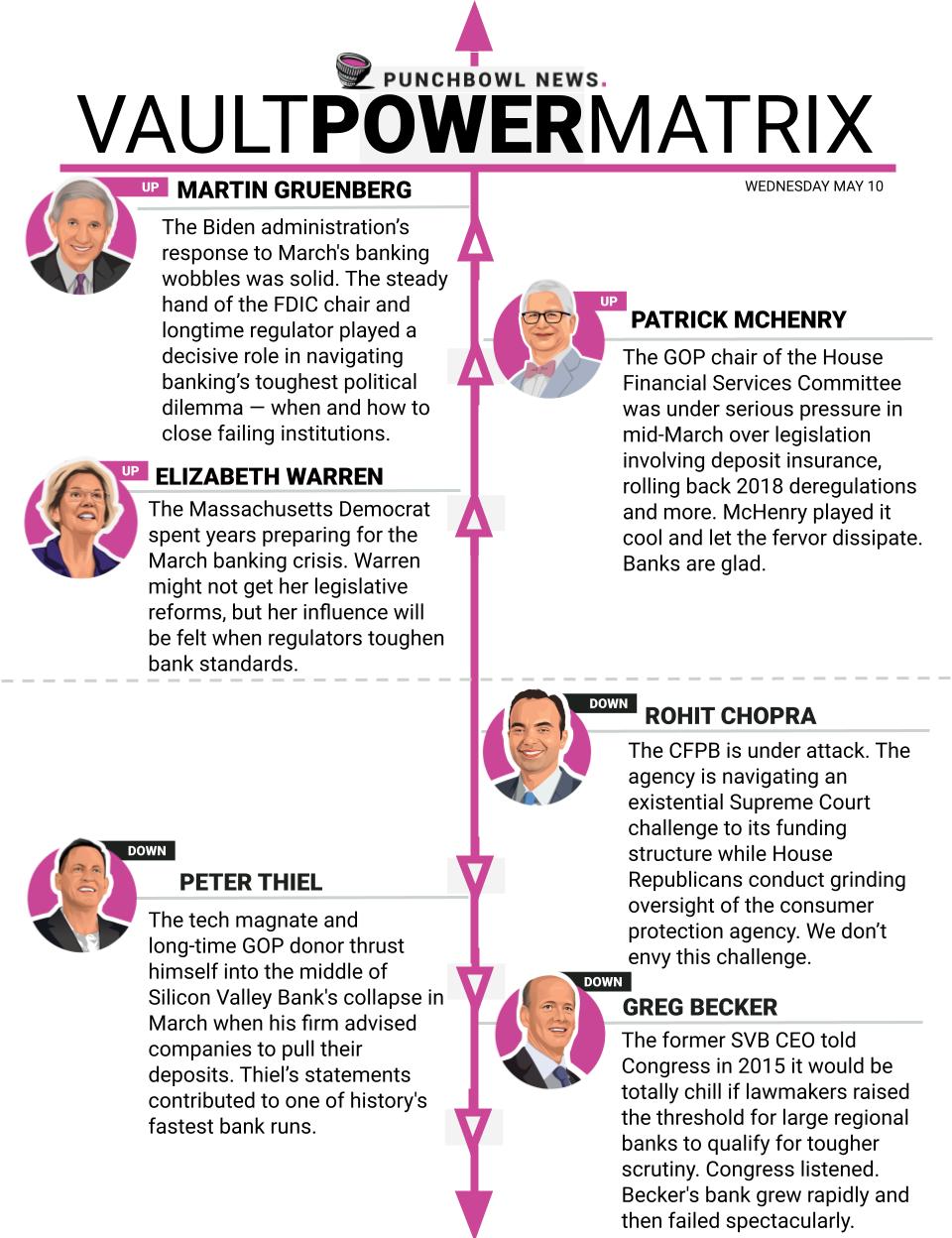

A fresh take on the Punchbowl News Power Matrix exclusively focused on the world of financial policy that definitely won’t make anyone mad.

A regulatory outlook that details Republicans’ long-term playbook as they go to war with financial regulators.

Questions or comments? Email us — [email protected] and [email protected].

We hope you enjoy our dive into the future of money.

– Brendan Pedersen and Jake Sherman

THE INTERVIEW

Jamie Dimon warns of debt limit ‘panic,’ urges calm on China

Jamie Dimon is the most powerful man in global finance.

When the 67-year-old CEO of JPMorgan Chase speaks, captains of industry, finance titans and Washington tend to listen. When the U.S. government needs a private sector lifeline, it often starts with Dimon.

Which is why we took note in a recent interview when he warned about the potential for a financial market panic as the U.S. hurtles towards a debt default.

President Joe Biden and Speaker Kevin McCarthy have just weeks to reach an agreement to raise the debt limit. Treasury projects the U.S. could default as soon as June 1, and the two left a meeting Tuesday with little sign of progress, save another meeting scheduled for Friday.

But even getting this close to the brink could be catastrophic, Dimon told us.

“This can cause panic. And you’ve seen, panic isn’t necessarily a rational thing,” Dimon said. “People panic. And [when] you see people panic — that’s ’08, ’09 again, and that’s really what you want to avoid.”

The potential for a financial market panic is not something Congress can legislate away as the X-date draws closer.

“I think there’s a higher chance of a mistake here because of the politics of the situation,” Dimon said. He also echoed warnings from policymakers like Treasury Secretary Janet Yellen that plenty of economic damage could be done well before the U.S. hits the X-date.

Here’s more from Dimon:

Dimon finds himself in a familiar spot as the banking crisis looms — in the thick of it. He was a key player in the $30 billion private sector effort to shore up First Republic in March. And it was Dimon’s bank that ultimately bought the regional bank this month.

As CEO of JPMorgan Chase since 2005, Dimon is now the longest serving chief executive of any American mega-bank. He’s also the only CEO still leading the same mega-bank since the U.S. economy limped away from the 2007-2008 global financial crisis.

Dimon’s public profile isn’t just a consequence of his job helming America’s largest bank. JPMorgan boasts roughly $3.7 trillion of assets, not including First Republic — a deal Dimon closed after speaking with Punchbowl News.

It’s because few bankers, if any, have ever played such a crucial private sector role in economic crises past and present.

Overall, Dimon could do without the debt-limit dramatics. “I hope we avoid it,” he said, referring to default. “I hope, one day, we get rid of it,” Dimon added, reiterating his call for a permanent end to the debt limit.

Unlike the serious Obama-era fights over the debt limit, the banking system today is grappling with instability. Regional banks remain under stress.

But in contrast to progressives in Congress and other critics of Wall Street, Dimon argues that Trump-era deregulation has not played a key role in the banking industry’s latest woes.

“We don’t believe that the problem was caused by that change in regulation that happened a couple of years ago,” Dimon said. He was referencing the 2018 bipartisan bill that eased some regulations around mid-sized banks, including higher asset thresholds for the toughest bank exams.

‘Tough but thoughtful’ approach to China: Dimon supports a bipartisan congressional approach to China but wants to make sure things don’t get too heated.

“I think [Congress is] putting proper attention to the issue. Now, some people are overly shrill about it,” Dimon told us. “America has still got the best hand ever dealt of any nation on the planet. Take a deep breath, focus on the issues.”

Dimon said he’s spoken with “many” lawmakers and policymakers in Washington about economic policy and China, and he thinks “they’re there, they’re on it.” He specifically commended key Biden officials like National Security Adviser Jake Sullivan, Secretary of State Antony Blinken, Commerce Secretary Gina Raimondo and Yellen.

What needs to be done now, Dimon added, is “you’ve got to get into treaties and forms and private conversation” with China.

Dimon is essentially calling for an American approach to China that’s “tough but thoughtful.” That’s another way of saying Washington shouldn’t be aiming for full-on economic war with Beijing, even as global competition for resources heats up in the coming years.

Dimon says a thoughtful approach has to start with a recognition that China, for all its might, is “not a 10-foot-tall soldier” when compared to the United States.

Here’s more from Dimon on China:

One last thing: We’re in the midst of another months-long news cycle where economic pundits wonder whether the world is on the verge of moving away from having the U.S. dollar as the global reserve currency. We’ve even heard some criticism of the long-running phenomenon from Republicans like Sen. J.D. Vance (Ohio).

Dimon’s take: You’re going to miss dollar dominance if and when it’s gone.

“The strength of the mighty dollar is predicated upon the strength of the United States economy, the tacit authority of the Federal Reserve Bank and the openness” of the dollar, Dimon said.

“Anyone who wants to weaken the dollar would weaken those other things, and that would be a bad idea for America,” he added.

– Brendan Pedersen

THE POWER MATRIX

Presented by AstraZeneca

![]()

The 340B program is supposed to help vulnerable patients—but without strong safeguards, it’s siphoning away funds that could be used for free and charitable medicine. The 340B Rebate Model Pilot improves program integrity, preventing duplicate discounts and strengthening accountability. Urge HHS to implement the pilot today. Learn why it matters.

Crucial Capitol Hill news AM, Midday, and PM—5 times a week

Join a community of some of the most powerful people in Washington and beyond. Exclusive newsmaker events, parties, in-person and virtual briefings and more.

Subscribe to Premium

Special Projects

Explore our deep dives into the issues that matter the most today and will shape tomorrow's future, with expert reporting that goes beyond the headlines and into the heart of the Capitol.

Check it outEvery single issue of Punchbowl News published, all in one place

Visit the archive

Presented by AstraZeneca

![]()

The 340B program lacks transparency—making it hard to tell if it’s actually helping vulnerable patients. HHS can fix the problem by implementing the 340B Rebate Model Pilot, ensuring the program is transparent, compliant, and accountable. Learn more.