The Archive

Every issue of the Punchbowl News newsletter, including our special editions, right here at your fingertips.

Join the community, and get the morning edition delivered straight to your inbox.

December 5, 2023

Read our latest series

Our newest editorial project, in partnership with Google, explores how AI is advancing sectors across the U.S. economy and government through a four-part series.

Check out our first feature focused on AI and energy innovation with Governor Youngkin.

PRESENTED BY

Welcome back to The Vault.

It’s been quite a few weeks — and year — for the global economy.

Bankers have been seriously worried about world politics since February 2022 with the Russian invasion of Ukraine. But the Israel-Hamas war has supercharged the feeling from Wall Street that the global economy’s health is less secure than it has been in decades.

That’s why we sat down with Treasury Secretary Janet Yellen, who has some thoughts about Congress’ role on the world stage these days.

As we’ve written elsewhere, the Treasury Department has spent months trying to convince members of Congress to continue supporting Ukraine’s war effort and humanitarian needs.

But for Yellen, the stakes of this fight — as well as the continuing crisis in the Middle East — are as much about short-term stability as the long-term economic trajectory of the United States and its allies.

In this edition of The Vault, we also take a closer look at the credit card wars. Banks have lobbied hard against the retailer-supported Credit Card Competition Act, but there’s widespread skepticism that the bill could ever pass. Is Wall Street right?

We’ll hear from top bank executives directly this week, when CEOs like JPMorgan Chase’s Jamie Dimon, Citigroup’s Jane Fraser, Wells Fargo’s Charlie Scharf, Goldman Sachs’ David Solomon and more testify before the Senate Banking Committee.

Finally, there’s crypto. This year has been a political rollercoaster for the sector as a long string of scandals continue to mire the industry’s reputation.

Some hoped former FTX CEO Sam Bankman-Fried’s guilty verdict in November would put the crypto-verse’s worst days behind it. Then, the U.S. government smacked international crypto firm Binance with an eye-watering $4 billion fine. We unpack how the sector hopes to drag itself back into Washington’s good graces.

Thanks as always for reading.

— Brendan Pedersen

Sign up to stay in the know with The Vault, Punchbowl News’ pipeline from Washington to Wall Street.

THE INTERVIEW

Janet Yellen on Ukraine, deficits and working with Speaker Johnson

More than two years into her job as the Biden administration’s top economic official, Treasury Secretary Janet Yellen must now contend with a House transformed partly by the election of the most conservative speaker in recent memory.

The relationship between Yellen and Speaker Mike Johnson is not off to a banger start.

News: Yellen said she hasn’t spoken to Johnson since he was elected six weeks ago. With all that’s happening in the U.S. economy and abroad, this is a bit of a shocker.

Moreover, the most notable legislative strategy Johnson has employed to date — tying Israel aid to IRS funding cuts — prompted swift condemnation from Yellen in a November address.

“His role is key, and we want to work with him to make sure we deliver for hardworking families,” Yellen told us, referring to Johnson. “I would, however, say that the one thing I was aware of that he did propose, which was cutting funding for the IRS, I would strongly object to. It’s very dangerous.”

Yellen might have the most jam-packed portfolio across all of the Biden administration. The wars raging abroad have only complicated the mix.

Yellen has the unenviable job of securing funds for Ukraine and the Middle East conflict, implementing historic climate and infrastructure investments and reopening economic talks with China. Not to mention, she’s also trying to sell President Joe Biden’s economic agenda to a persistently skeptical public.

A longtime public servant and former chair of the Federal Reserve, Yellen is well-positioned to navigate these challenges. But Congress has not made her job any easier, especially lately.

Ukraine aid: Treasury has directed a full-court press toward Congress in the hopes of shoring up political support for another multi-billion dollar supplemental request for Ukraine.

“They’re bracing for a long winter,” Yellen said of Ukraine. “And this is support that is critical for them to be able to continue to be engaged in the war effort.”

But Yellen’s push comes as support for the war is waning among Republicans. Throughout our conversation, Yellen pointed out that the United States was “not doing this alone,” citing a broad international coalition sending money to Ukraine.

We asked Yellen whether she was concerned this latest supplemental request for Ukraine could be the last Congress approves – if lawmakers can pass it at all. She replied:

For Yellen, the goal is to send “critical” funding for broader economic aid, not just military backing.

“Ukraine is currently spending every penny or more that it takes in revenue for military purposes, to support its war effort,” Yellen said. “So we’re filling in money that they need for government functions like hospitals, first responders, school teachers.”

The deficit: Yellen acknowledged a shifting financial environment could force policymakers to grapple with the economic effects of the United States’ $33 trillion national debt more quickly.

Interest rates are up. And recent stress in the bond market, coupled with yields near historic highs, has left policymakers wondering whether federal payments on U.S. debt could soon introduce a real drag to the economy’s long-term growth. The United States spent $659 billion on bondholder payments in FY2023, nearly double FY2020’s total of $345 billion.

Yellen argued the Biden administration is taking the deficit seriously, citing budget proposals that would reduce the deficit by a few trillion dollars over the next 10 years.

But also she said a persistent elevation in interest rates would create “a somewhat greater challenge” for policymakers.

“Additional deficit reduction is appropriate,” Yellen said. “The president has proposed that and would stand ready to work with Congress to look for ways to enact that.”

Stablecoins: Yellen echoed concerns from congressional Democrats about one of the key planks of House Republicans’ approach to crypto reform. For years now, the Treasury secretary has asked Congress to pass legislation regulating stablecoins, arguing the product could pose unique financial stability risks.

But Yellen told us it was vital for the federal government to play an oversight role. The Republican approach would limit the Federal Reserve’s direct supervision over state-chartered stablecoin companies.

“It’s critical that the federal government essentially has a role in providing a floor for what is an acceptable state of regulation with respect to stablecoins. I’m not comfortable with the idea of only state regulation and no federal role,” Yellen said.

Lawmakers supportive of the House’s stablecoin bill say it introduces a federal floor. But opponents have argued there are outstanding questions about how those standards would be enforced by state authorities.

Big fiscal: Debt concerns notwithstanding, Yellen said she was increasingly sure the Biden administration’s “go big” fiscal response to the pandemic was the right approach.

There’s been a lot of debate in Washington about whether federal spending in 2020 and 2021 fueled inflation in 2022. Yellen thinks recent economic developments are evidence that inflation was truly transitory.

Yellen told us she believed the American Rescue Plan was the correct response and that the recent dropoff in inflation figures has made her “feel more confident” about that assessment.

— Brendan Pedersen

PRESENTED BY GOLDMAN SACHS 10,000 SMALL BUSINESSES VOICES

Only 29% of small business owners can afford to take out a loan given current interest rates.

Small business owner Dr. Shantell Chambliss, CEO of Nonprofitability in Richmond, VA: “It’s not that we’ve been denied, it’s that the terms would hurt our business more than help.”

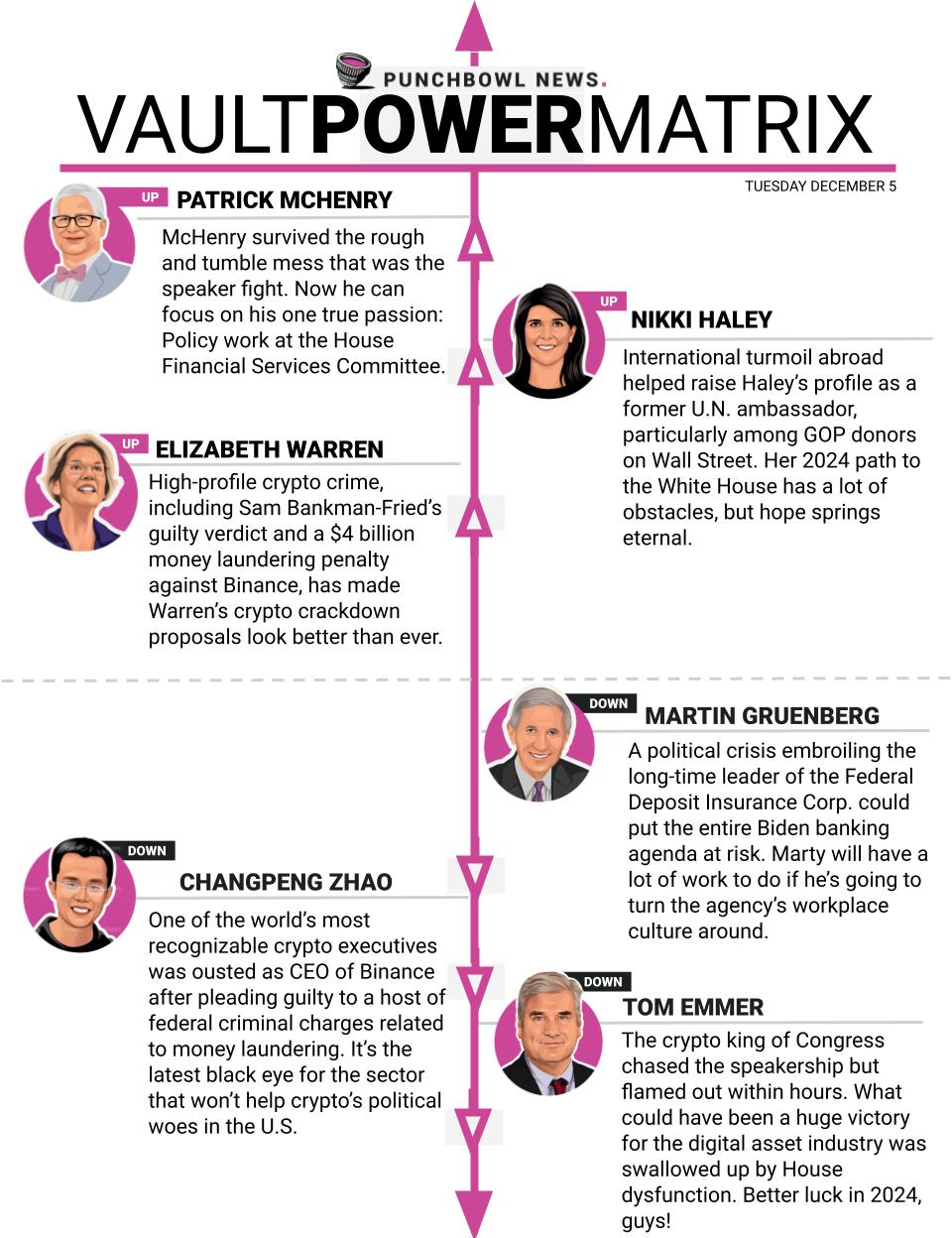

VAULT POWER MATRIX

— Brendan Pedersen

PRESENTED BY GOLDMAN SACHS 10,000 SMALL BUSINESSES VOICES

Tell the Fed: Stop the Squeeze on Small Businesses

The Fed’s proposed bank capital requirements will make it harder for minority-owned businesses to access capital.

| → |

| → | Only 26% of Black small business owners that applied for business loans or credit in the past year received their requested funding amount. |

“The capital that I’ve been able to secure was very expensive,” says Ceata Lash, CEO of PuffCuff in Marietta, GA. “And now I’m paying for it.”

Crucial Capitol Hill news AM, Midday, and PM—5 times a week

Join a community of some of the most powerful people in Washington and beyond. Exclusive newsmaker events, parties, in-person and virtual briefings and more.

Subscribe to Premium

The Canvass Year-End Report

And what senior aides and downtown figures believe will happen in 2023.

Check it outEvery single issue of Punchbowl News published, all in one place

Visit the archive

Read our latest series

Our newest editorial project, in partnership with Google, explores how AI is advancing sectors across the U.S. economy and government through a four-part series.

Check out our first feature focused on AI and energy innovation with Governor Youngkin.